The time geography equation- understanding where 5G FWA truly wins

5G Fixed Wireless Access (FWA) is reshaping how households and businesses get online. Operators are launching it at scale, customers are adopting it quickly, and in many countries, it’s starting to shift competitive dynamics. Yet the industry conversation still tends to focus on speeds, prices, or coverage and in doing so, it often misses a far more important structural driver.

Time and geography are decisive factors in fixed broadband strategy often making 5G FWA the pragmatic choice, though not in every context. This is the essence of the Time-Geography equation, a simple way to explain why FWA thrives in some markets, complements fibre in others, and stays niche elsewhere.

Where time becomes the deciding factor in broadband deployment

Traditional broadband decisions revolve around capacity, reliability, and cost. These matter but in real deployments, time to market often becomes the factor that determines who wins and who falls behind. Time to market here simply means how quickly an operator can get a live connection to a customer.

Deployment fundamentals: 5G FWA vs. fibre

5G FWA: Uses existing mobile sites and spectrum. The last mile travels over the air, so getting customers online can be quicker and often avoids an engineer visit (unless outdoor CPE is needed).

Fibre: Requires new physical last mile build. Permits, access to premises and inhome installation (ONT) add complexity and time especially in dense areas, distances stretch timelines outside them.

Where operators already have extensive fibre, service activation is quick and time‑to‑market is less differentiating. FWA retains a convenience edge by avoiding in‑home engineer visits (unless outdoor CPE is required), whereas a new fibre line entails an ONT install. As more homes already have ONTs, that friction continues to fall.

FWA’s advantage shows up most clearly in situations where operators need to move fast, and where customers do not demand full fibre-like speeds.

Deploying fibre remains engineering heavy, trenching, permits, inspections, workforce, last mile complexities, and weather delays. Even in mature markets, this takes months, in large geographies, sometimes years.

Delays have practical consequences:

Customers churn when installation slips from days to weeks.

Operators lose share if competitors activate service faster.

The result is that FWA transforms broadband deployment from a civil works problem into a logistics problem. And that it is easier to scale logistics than construction. If fibre is the long-distance runner of infrastructure, FWA is the sprinter, it wins every short race where speed to connect matters. In markets where time to connect defines competitiveness, FWA does not just complement fibre it overtakes it.

How geography shapes broadband economics

If time determines urgency, geography determines feasibility. Every market, its density, terrain, and cost structures shape whether an operator leans more on fibre, wireless, or a mix of both.

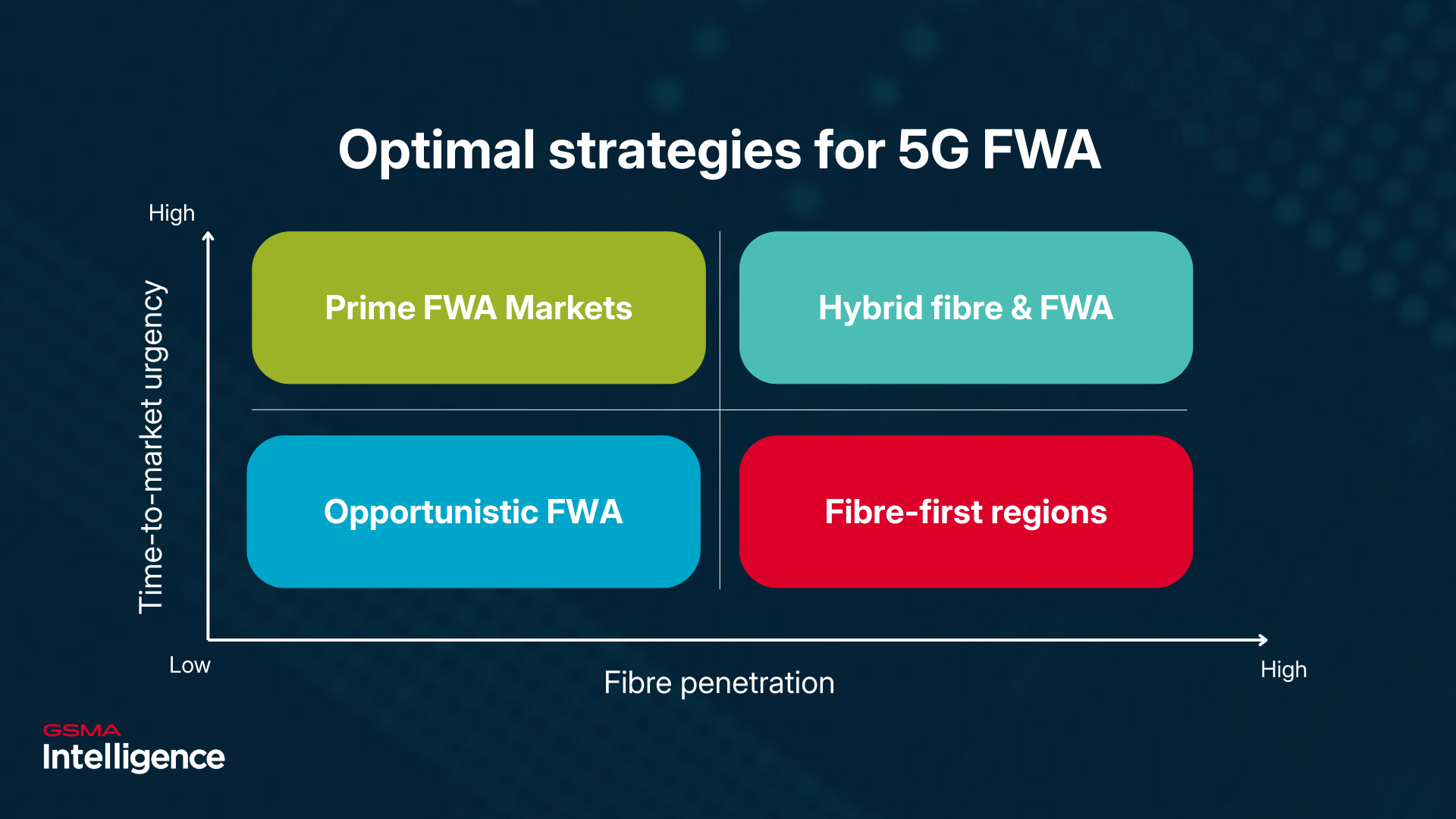

Most countries fall into one of four strategic profiles.

1. Prime FWA markets (High time to market and low fibre penetration): These are markets where rolling out fibre is slow, expensive, or geographically constrained and operators need a faster way to turn on broadband for example, USA and India.

Large landmass with significant gaps beyond metro areas

Challenging terrain, e.g. mountains, small islands, etc.

FWA acts as both a coverage tool and a competitive differentiator

2. Hybrid fibre + FWA markets (High time to market and high fibre penetration): These markets have strong fibre cores, but timelines and cost challenges at the edge make hybrid strategies more efficient.

Fibre dominates dense cities

FWA accelerates suburban and rural expansion

3. Opportunistic FWA (Low time market and low fibre penetration): Where FWA is not a primary broadband strategy but solves specific use cases. FWA serves mining sites, temporary camps, remote communities and can provide backup connectivity, which is particularly attractive for enterprises.

4. Fibre first regions (Low time to market and high fibre penetration): Fibre economics are strong, populations dense, and timelines less pressured. Example, South Korea.

Among the world’s highest fibre penetration rates

FWA exists but plays only a small complementary role primarily for back-up / temporary connectivity)

Conclusion: FWA isn’t replacing fibre, it’s redefining connectivity strategy

The success of 5G FWA is not about superiority. It is about suitability.

Fibre will remain the long‑term foundation of fixed broadband. But fibre cannot always move fast, and customers do not always want to wait. In many markets, FWA fills the time gap, accelerating coverage, expanding reach, and giving operators strategic flexibility that heavy civil infrastructure cannot.

Fibre is the backbone. FWA is the accelerator. Used together, they allow operators to build networks that are not only fast, but also responsive, agile, and aligned with real‑world deployment constraints.

As digital demand rises and geography continues to shape investment decisions, operators’ strategies designed and aligned with the Time–Geography equation will be best positioned to lead the next decade of broadband growth.

For a more detailed view of global fixed broadband and FWA developments, including forecasts, trends and copper sunset, check out our latest Fixed Broadband and FWA Markets, Q3 2025: developments and outlook report here.

Author

- 200 reports a year

- 50 million data points

- Over 350 metrics

How can we support you?

Get in touch

Contact the GSMA Intelligence support team for help with your account, subscriptions, or access to reports and insights.

Newsletter

Subscribe to the GSMA Intelligence newsletter for the latest industry news and insights, delivered to your inbox.