Are we seeing another dot-com moment? What the AI investment cycle means for telecom

By Harry Aquije Ballon, GSMA Intelligence & Luis Ortiz Chavez, External co-author

The surge in equity markets since 2023, led by technology firms at the centre of artificial intelligence (AI), has prompted inevitable comparisons with the late 1990s. Valuations have risen sharply, capital expenditure is accelerating and expectations of transformative productivity gains are again shaping investor sentiment. For telecom leaders, the key question is whether this represents a repeat of the dot-com bubble or a more fundamental shift in the digital economy - one that will require stronger networks, advanced 5G and future 6G capabilities, and integration beyond traditional connectivity models to support a new generation of AI-enabled applications.

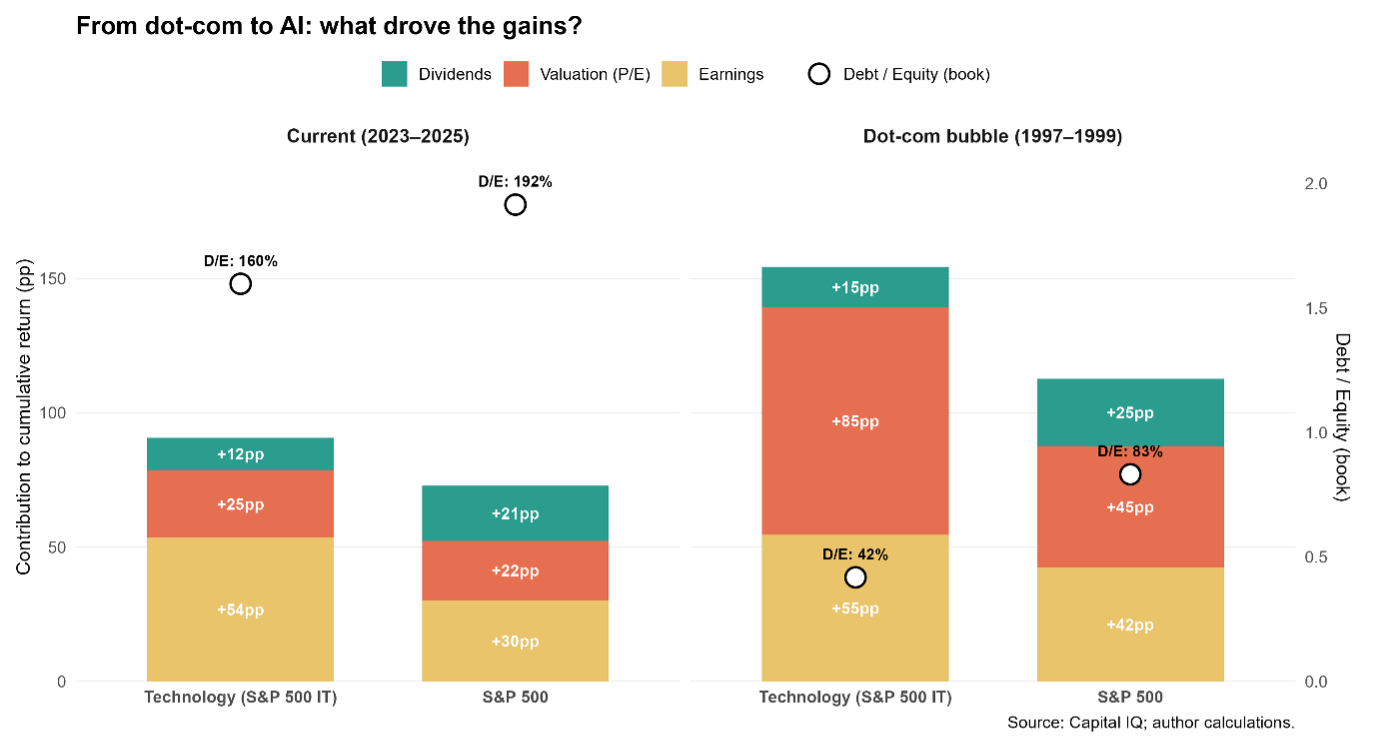

To assess this, in this article we compared the current AI-driven rally (2023–2025) with the dot-com boom (1997–1999), using firm-level data from Capital IQ for the S&P 500 and the S&P 500 Technology sector. Rather than focusing on headline index performance, we decomposed cumulative returns into three components: dividends, valuation expansion (P/E multiples) and earnings growth. This allows us to distinguish between gains supported by underlying profitability and those driven primarily by rising investor expectations. The decomposition highlights a clear contrast between the two periods.

During the dot-com boom, valuation expansion played a dominant role, particularly within the technology sector. Multiples rose rapidly relative to earnings, reflecting expectations that far outpaced realised profitability. In the current AI cycle, the picture is different. While valuations have increased, the majority of returns since 2023 have been driven by earnings growth. This is especially evident within the technology sector, where stronger profitability has accounted for a significant share of cumulative gains. On this measure, today’s rally appears more fundamentally anchored than that of the late 1990s.

However, the balance sheet context is materially different.

When we examine leverage using Capital IQ’s aggregate Debt-to-Equity (book) ratios, we find that corporate leverage - the extent to which companies finance themselves with debt relative to equity - is substantially higher today than during the dot-com period, across the S&P 500 and the technology sector. This does not imply immediate instability; many firms today operate with larger, more diversified revenue bases and stronger cash generation. Nevertheless, it changes the risk profile. If earnings growth were to slow or expectations adjust, corrections would unfold in a more leveraged environment.

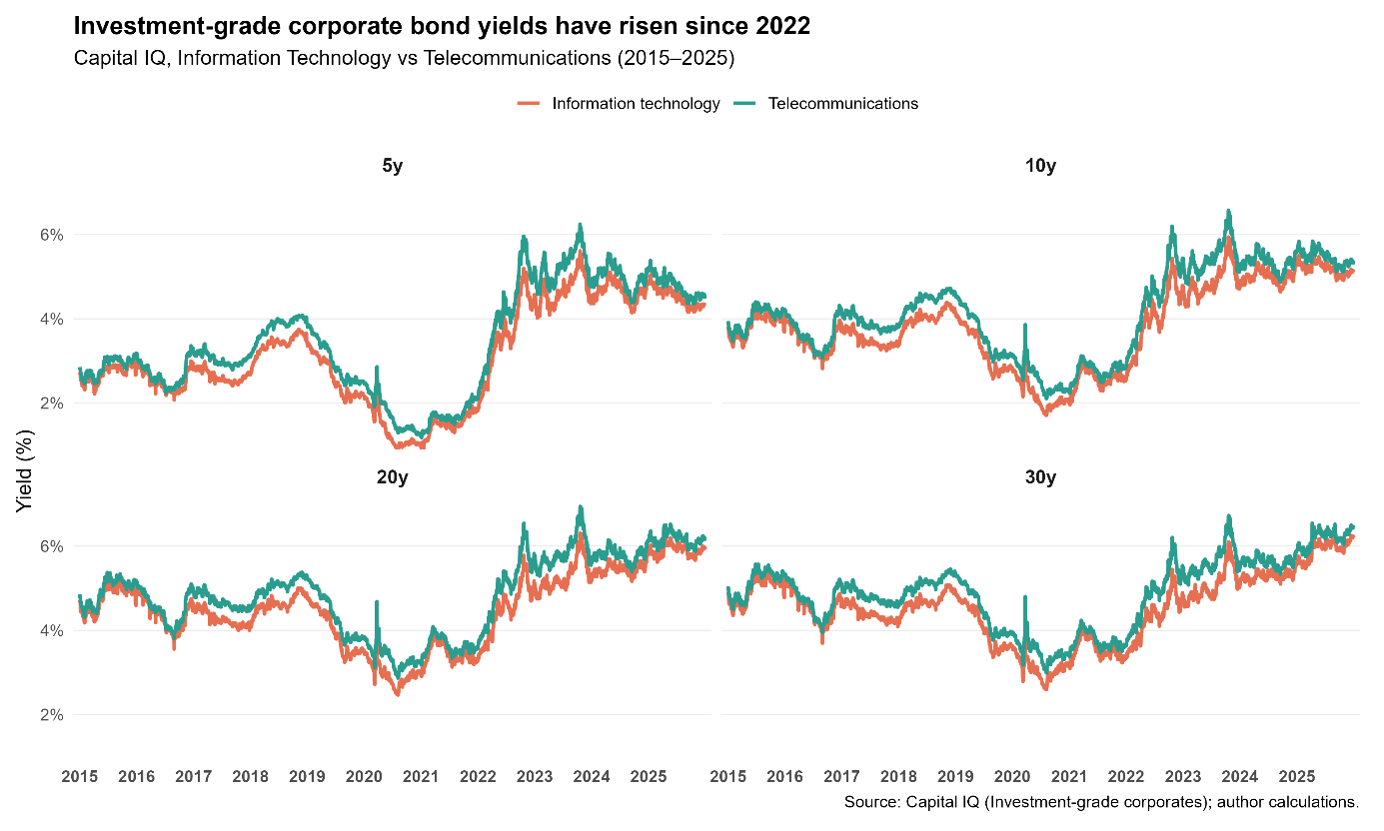

The cost of that leverage also looks very different today. The chart below compares investment-grade corporate bond yields for information technology and telecommunications firms across maturities from 2015 to 2025. Unlike the relatively moderate rate environment of the late 1990s, the current AI investment cycle is unfolding amid tighter monetary conditions. Since 2022, corporate bond yields have risen markedly across maturities, increasing the cost of funding for capital-intensive sectors.

This distinction is particularly relevant for telecom. Unlike the dot-com boom, which was largely centred on software and internet platforms, the AI cycle is infrastructure-intensive and spans multiple technological layers, including energy, semiconductors, models and applications. Expanding AI capabilities requires sustained investment in cloud capacity, advanced chips, data centres and high-performance connectivity. Fibre and satellite backhaul, 5G networks and edge infrastructure are foundational to supporting AI workloads. Telecom operators therefore sit at the core of this investment wave.

At the same time, higher leverage combined with more expensive debt raises important strategic questions.

AI-related capex is significant and ongoing. If financed through increased borrowing, balance sheet resilience becomes more critical in an elevated rate environment. For telecom operators, already capital-intensive and often highly leveraged, higher corporate yields raise the hurdle rate for investment decisions and narrow financial flexibility. While AI presents long-term demand opportunities for connectivity providers, the financial conditions surrounding this expansion are materially tighter than during previous technology booms.

More broadly, what differentiates the current cycle is the maturity of the technological ecosystem. AI builds on decades of research and has reached commercial scale through exponential increases in computing power and complementary digital technologies. Adoption has been rapid, although productive integration — where AI tangibly reshapes workflows and drives efficiency gains — remains uneven across sectors. Even so, AI applications are already generating measurable improvements in areas such as enterprise software, manufacturing and healthcare, where deployment is increasingly linked to auditable outcomes. In contrast, the dot-com era was characterised by early-stage internet adoption and evolving monetisation models. Today’s expansion rests on more developed infrastructure and clearer revenue pathways, even if expectations remain elevated.

For telecom, the opportunity is significant. AI-driven demand for data processing, cloud integration and low-latency connectivity reinforces the strategic role of networks in the digital economy. The evolution of 5G and the roadmap toward 6G will be central to supporting these applications. Realising this potential will require coordination between operators, technology firms and governments to ensure that infrastructure investment translates into sustained productivity gains.

The evidence suggests that the current rally differs meaningfully from the dot-com episode. Earnings growth, rather than multiple expansion alone, has driven recent gains. Yet leverage is materially higher than in the late 1990s, introducing a distinct financial constraint. The lesson is not that AI resembles a speculative bubble, but that innovation cycles unfold within specific financial conditions. For telecom leaders, the challenge is to capture the structural upside of AI-driven demand while maintaining investment discipline and balance sheet resilience in a more leveraged corporate landscape.

- 200 reports a year

- 50 million data points

- Over 350 metrics

How can we support you?

Get in touch

Contact the GSMA Intelligence support team for help with your account, subscriptions, or access to reports and insights.

Newsletter

Subscribe to the GSMA Intelligence newsletter for the latest industry news and insights, delivered to your inbox.