Reaching for the sky: From partnerships to commercial realities in satellite connectivity

Satellite communication continues to grow in prominence as a complement to terrestrial networks. Last year, the focus was on partnerships. At the time of IMC 2024, a total of 91 operators/operator groups – representing 61% of the global mobile market by connections – had active partnerships with one or more satellite players. Fast forward to today and the conversation has shifted. With larger constellations in orbit (expanding the existing constellations and launch of new constellations) and successful trials, these partnerships are now moving into commercial action. This article builds upon the views I shared in my IMC 2024 piece, reflecting on how the satellite connectivity landscape has evolved and what this means for India’s satcom journey.

Why India matters in the satcom story

For a market like India, satellite connectivity holds undeniable importance. The country still has a large population base (approx. 400 million) either not covered by mobile internet services or underserved (the usage gap). This is even more pronounced in rural parts of the country, where government data shows internet penetration at just 46 subscriptions per 100 people. The country has over 600,000 villages, many in remote or hard-to-reach locations where fibre rollout remains slow and expensive. As such, satellite connectivity offers an efficient way to extend coverage and overcome backhaul limitations in these locations.

While this scenario is particularly stark in India, the same story resonates globally: connecting the final 5–10% frontier remains economically challenging with terrestrial networks, making satellite a viable alternate.

2024 vs 2025: From partnerships to services

By the end of September 2025, a total of 110 operators/operator groups (91 at IMC 2024)- representing 67% of the global mobile market by connections – had active partnerships with one or more satellite players. While this is only a modest rise from last year, it also means two-thirds of the global mobile market is now engaged. The real shift, however, has been in commercial launches. The number of operators with live satellite services has nearly doubled, from 16 to 28 in a year, signalling the move from trials to reality.

Operators are now reporting tangible progress too. KDDI in Japan has reported more than 1 million customers on satellite connectivity. One New Zealand also reported that its customers have already sent over 1 million SMS messages using satellite links. In other parts of the world, Vodafone and AST SpaceMobile have established a joint European HQ in Luxembourg to scale direct-to-device (D2D) services. Notably, D2D-focused telco-satellite partnerships (excluding satellite broadband) have grown from 45% to 58% year-on-year, underscoring both ecosystem development and rising consumer appetite for ubiquitous coverage.

In India, however, backhaul connectivity remains as critical as D2D given the rural–urban divide.

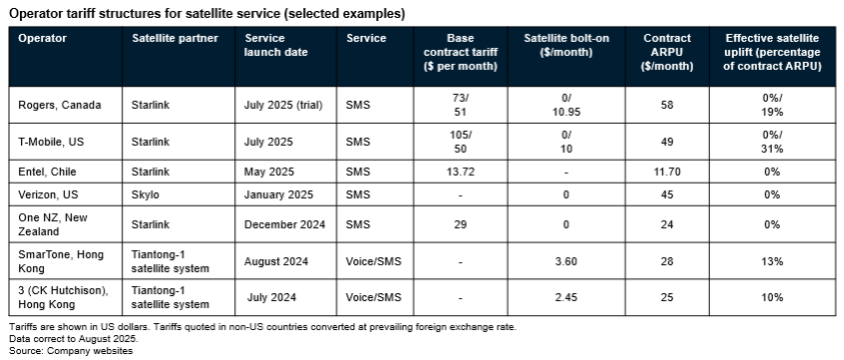

Monetisation: From estimates to evidence

A GSMA Intelligence survey in June 2024 across 10 countries suggested a 5–8% ARPU uplift based on consumer sentiment. With operators now rolling out satellite services and tariffs (some of which are shown below), the picture is clearer. Hybrid models are emerging: some include satellite as a bundled benefit for premium customers, while others charge separately. Early evidence points to the potential for ARPU uplift of up to 20%, depending on the country and tariff strategy. Adoption, however, is likely to be staggered due to handset replacement cycles and limited consumer awareness

Enterprise opportunities are also widening. A GSMA Intelligence–Skylo survey this year found that 20% of businesses face daily operational disruptions due to unreliable connectivity. Existing solutions have fallen short, creating space for satellite alternatives. GSMA Intelligence projects an additional USD 10 billion annually from enterprises by 2035, driven by up to 2 billion IoT connections supported through satellite.

India’s satcom landscape today

The importance of satellite connectivity in complementing terrestrial networks in India is evident not only in operator–satellite partnerships but also in rising investments. Bharti Airtel holds a majority stake in Eutelsat OneWeb, while Reliance Jio has formed Orbit Connect India with SES to deliver satellite broadband. BSNL has launched direct-to-device (D2D) services with Viasat. In June 2025, Starlink became the third licensed player after OneWeb and Inmarsat.

With every telco tied to an active satellite partner, BSNL’s service launch, and Starlink’s entry, India’s immense potential in satellite connectivity is clear.

So what? Looking ahead

The shift from partnerships to commercial services marks a key step in making satellite connectivity mainstream. The first wave has centred on SMS and, in some cases, voice. Over the next few years, services will expand into data, supported by better latency and performance for existing offerings. KDDI, for example, plans to launch satellite-enabled data later this year and enhance SMS delivery speeds.

Monetisation models are also evolving. Early results show strong ARPU uplift, but operators will need to refine pricing as adoption grows. For regulators, spectrum remains a critical piece of the puzzle, with key decisions expected in the lead up to WRC-27. However, there will be spectrum capacity constraints in the near-term and partnerships will continue to explore various models, such as Echostar and SpaceX deal.

Ultimately, the question has shifted from whether satellite can complement terrestrial networks to how quickly and effectively it can be scaled. With commercial launches under way, enterprise demand increasing, and India positioning itself at the centre of the story, it will be interesting to see how next two years unfold.

Author

- 200 reports a year

- 50 million data points

- Over 350 metrics

How can we support you?

Get in touch

Contact the GSMA Intelligence support team for help with your account, subscriptions, or access to reports and insights.

Newsletter

Subscribe to the GSMA Intelligence newsletter for the latest industry news and insights, delivered to your inbox.